How a Soft Landing for the Economy Could Boost Bitcoin

With interest rates falling and recession risks remaining moderate, the perfect setup might be forming for Bitcoin's next rally.

Welcome to MrGekkoWallSt's virtual office! This is edition number 11 of my newsletter! Here, I organize and share my insights on the market, technical analysis, education, experiences, reflections, and the most relevant news of the period.

Real GDP Continues Moderate Growth

The United States' real Gross Domestic Product (GDP), on an annualized basis, grew by 2.8% in 2024 compared to the previous year. This result underscores that the economy remains, for now, far from a recessionary scenario, despite ongoing uncertainties in the global macroeconomic environment.

Annual growth in real GDP boosts confidence and drives job creation, tax revenues, and investment. On the flip side, when real GDP is declining, investors begin to question the government’s fiscal sustainability, demanding higher returns to compensate for increased risk—putting upward pressure on interest rates.

This environment of uncertainty and reduced liquidity tends to negatively impact risk assets such as stocks and cryptocurrencies, as capital typically flows toward safer investments.

The main real GDP growth forecasts for 2025 are 1.8% according to the IMF and 1.7% according to Fitch Ratings, with expected inflation at 4.3%. Based on Fitch Ratings’ projection, nominal GDP growth will be 6%, reflecting economic activity that is expected to remain strong despite inflationary challenges.

Confirmation of a possible recession (if the annual real GDP growth for 2025 turns out negative) will only be possible in April 2026, when the full data for the year is released.

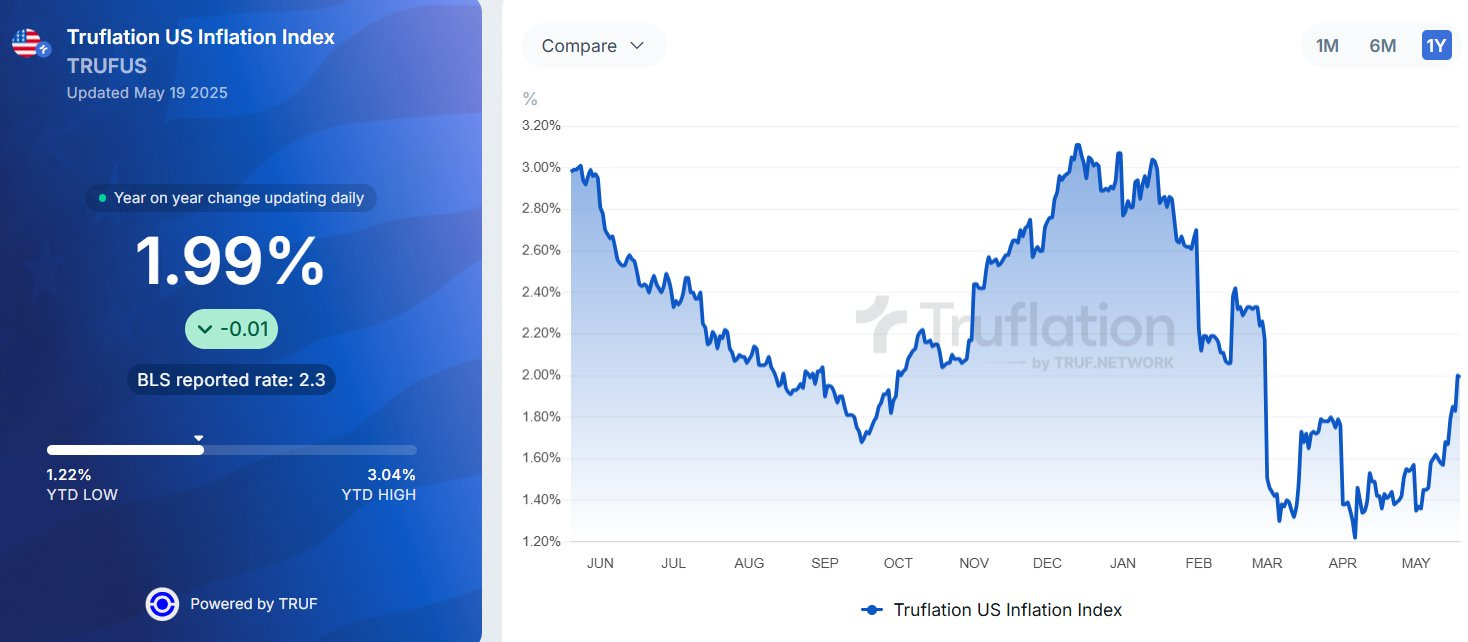

Inflation Below 3% with a Stable Trend

The Consumer Price Index (CPI) for May came in at 2.3%, keeping inflation on a sideways path below the 3% threshold. In April, following the recent implementation of Donald Trump’s tariff policy, real-time inflation data continued to show declines, although this trend has yet to be fully reflected in the government’s lagging indicators.

However, in the past few days, real-time inflation has started to rise. Could this be the result of tariffs impacting the supply chain?

Although real-time inflation accelerated in May, it’s important to remember that the impact of tariffs is typically a one-time event. When a tariff is imposed, it immediately raises the import cost of that good, which then gets passed on to consumer prices. However, this effect happens only once — meaning prices jump to a new level but don’t keep rising indefinitely just because of the tariff. This differs from sustained inflation, which requires ongoing price increases.

As long as there isn’t a significant distortion caused by aggressive monetary expansion, the disinflationary trend is likely to resume in the short to medium term — especially since the Federal Reserve (Fed) has not yet ended quantitative tightening (QT) and continues to keep interest rates (Fed Funds rate) elevated. These factors are expected to keep consumer confidence and risk appetite subdued.

Tariffs can contribute to a renewed upward pressure on inflation as measured by the CPI. However, the inflationary impact will heavily depend on the extent of economic deterioration. Without a major distortion from aggressive monetary expansion, the current disinflationary environment is likely to persist in the near to mid-term, mainly because the Fed hasn’t yet stopped QT and still maintains high interest rates.

The recent rise in real-time inflation, combined with uncertainty around the end of quantitative tightening, prolongs the window of uncertainty. Within this window, the most favorable scenario for risk assets (stocks, crypto, etc.) would be if the inflation caused by tariffs proves to be a one-off effect, without persistence.

Then, when the Fed eventually reverses its monetary policy, the inflationary impact of that shift will also heavily depend on how much the economy has weakened by that point — because the weaker the economy, the more capacity it has to absorb inflation, and the less worried investors would be going forward.

Long-Term Treasuries with Elevated Yields: Two Competing Narratives

The 10-year Treasury yield remains around 4.30%, showing resilience against a decline, and two narratives are gaining traction:

Geopolitical Pressure: China may be selling U.S. Treasuries in response to U.S. tariff policies, increasing risk perceptions and pushing yields higher.

Unwinding of Basis Trades: The closing out of arbitrage positions in the Treasury market could be temporarily preventing yields from falling.

It’s likely that Treasury yields aren’t dropping because of the unwinding of basis trade positions. In other words, this doesn’t seem related to the narrative that China is dumping bonds as retaliation against the U.S., nor to the argument that the market is pricing in a debt default.

The second theory, related to basis trades, appears to better reflect the current situation. If confirmed, this could signal a medium-term trend of falling real interest rates, which lowers the cost of capital, increases the present value of future cash flows, and encourages a search for higher returns in assets like stocks, private credit, and even cryptocurrencies. You can learn more about this here:

Fed Nearing End of QT, Hints at “Stealth QE”

There are signs that the Fed is close to ending quantitative tightening (QT) by the end of the third quarter, with the possibility of then initiating a “stealth QE.” In short, to absorb the supply of Treasury securities, the Fed may pause QT and restart its quantitative easing (QE) program, while also granting a Supplementary Leverage Ratio (SLR) exemption for banks.

With QE, the Fed can print money and buy government bonds, expanding credit availability. The SLR exemption allows commercial banks to acquire these securities with virtually unlimited leverage, which also increases the overall credit in the economy.

The Fed and the banking system have the power to create money out of thin air, and both restarting QE and granting the SLR exemption are decisions solely under the Fed’s control. This increase in liquidity and credit tends to boost demand for risk assets, supporting their performance.

Labor Market Shows Stability

One possible explanation could be the increase in bank credit available to businesses and retailers, which stimulates the economy and helps maintain employment levels in the short term.

Many see the Fed at a crossroads between curbing unemployment and controlling inflation. However, as previously noted, inflation seems to be the lesser concern at the moment, which could soon open the door for stimulus — effectively lowering the risk of a sharp rise in unemployment.

Final Thoughts:

Given this, the current outlook presents two possibilities: a moderate recession that will be recognized only in hindsight, or a delay in the recessionary cycle — the so-called "soft landing."

The general assumption is that GDP in 2025 will show positive growth, with inflation and unemployment kept under control. The combination of these factors makes the possibility of a soft landing quite relevant.

In a soft landing scenario with stable macroeconomic fundamentals, risk assets tend to perform well in the short to medium term, especially if the market believes that the worst of monetary tightening is behind us and that central banks may eventually ease monetary policy.

Relevant News:

Macroeconomy:

Cryptocurrencies: